We have been investing for 4 years now, and have recently gone through a major paradigm shift. We haven’t fully switched to the new strategy yet, but I want to lay both out so where we’re at is clear. Then I’ll explain how we are going to proceed in the future.

I started my investment journey reading Money: Master the Game by Tony Robbins. That’s how I learned some of the most important investing lessons. Like how expensive 401k plans can be, or how actively managed mutual funds perform worse than the market most of the time and charge crazy fees (1-2% per year).

The most important thing I learned about was index funds and how powerful they are. Specifically the stock market index funds. Index funds are as important an innovation as compound interest in my opinion. It allows anyone to own the most successful companies in the country in one simple fund. They have tiny expense ratios because it’s a passive model, which is a huge part of why they’re so great.

Not only that but the concept of an index is self cleansing. Companies fight for market share and constantly try to beat each other. The winners rise and the losers fall. Innovations sweep across industries and change the landscape, disruptions break up dominating companies and chaos ensues. All the while the owner of the index sits above the fray and profits from all of it.

The book includes Ray Dalio’s all weather portfolio and thats what convinced me to get some money in the game. I had been scared to invest thinking that another market crash like 2008 was right around the corner. The safety of the money invested was of pramount importance. I didn’t know much about investing and I didn’t know where to begin, but I wanted to be safe. What I realize now was that I was scared because I didn’t know what I was doing, but more on that later.

What the all weather portfolio promises is a smooth ride. Not huge gains year to year, but no terrible losses either.

The concept seems very attractive and logical. Basically you balance your risk between 4 different financial conditions, high inflation, low inflation, strong economic growth and weak economic growth. The idea is that the market will be in 2 of those conditions at any given time so you have some investments that do well in all environments. The percentages break down like this:

- US Large Cap 12.5%

- US Mid Cap 5.5%

- US Small Cap 3.0%

- International 6.0%

- Emerging 3.0%

- Long Gov Bond 20.0%

- Intermediate Gov Bond 15.0%

- TIPS 20.0%

- Diversified Commodity 7.5%

- Gold 7.5%

I could go deeper into how this strategy works, but I’m going to save it for a later post. If you’re interested let me know!

So I had been investing in that strategy since 2017. My account had grown steadily over the years, not as much as the market did, but smooth and steady.

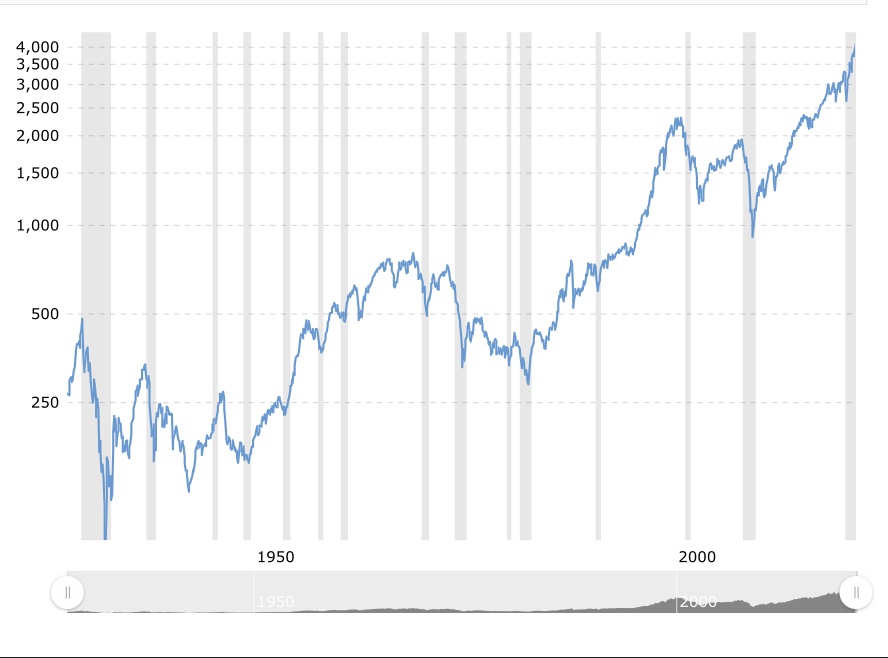

The first time I began to have some doubt was 2020. Covid hit the US hard in March and stocks fell off a cliff. By the time we reached the bottom of the bear market my portfolio had dropped by 19% while the total market dipped 28%. There’s that protection at work right?

At this point I was furloughed from work and since I was reasonably satisfied with the results of the portfolio I proceeded to put as much as I could into investments.

I was fortunate to receive unemployment early and without interruption. As our expenses were greatly reduced while quarantined my account grew at an impressive rate. That combined with the big bounce back accelerated my portfolio growth. Everything seemed great, until I started digging deeper.

It started as a thought experiment, I had met so many people who didn’t know much about investing and I wanted to help show how easy it could be. I settled on suggesting that people could just invest in an s&p 500 fund in a Roth. That simple plan would work really well. I posted the idea on social media and asked for feedback. I expected the idea to be controversial, but it wasn’t. Everyone seemed in support, and suggested other resources that advocated the same idea.

That’s when JL Collins book “A Simple Path To Wealth” was shown to me. What an amazing book. You can get the same lessons from his Stock Series here. It advocates investing primarily in the vanguard total market fund VTSAX and just toughening it out during the dips. That was in stark contrast to Tony Robbins’ book that assumed the dips would be too stressful for the average person.

As I thought about this I felt inertia from my previous way of thinking. It’s really hard to admit you’ve misjudged your strategy, especially when you’ve put so much thought and effort into it.

However JL Collins made sense. I had just proved I had the correct way of thinking during market dips, I got excited instead of scared when I saw the market falling by so much during covid. And I reaped the rewards so strongly that the lesson was ingrained deeper.

So I thought “I’ll start a small portion of my portfolio that invests in the total market index, and leave the rest in my all weather”. That’s where the idea of “Plan Z” came from. Just invest $100 per month in the total market index, never sell, and you’ll end up with over $400,000 in 40 years. It’s low risk, high reward, and anyone can do it. No matter your risk tolerance, since you’re not staking your whole future on it. It’s just a nice prize at the end of the rainbow.

So I thought the matter was settled. Then i got the app Personal Capital (which is awesome, like mint but better resources for investors). In the app it has a section called “You Index” which tracks your investing progress against other market indexes. That’s when I realized the mistake I was making.

While the total market index does bounce up and down, the fluctuations were still miles above my portfolio. I was striding the line between total stock index and total bond index. Which blew a hole in my thinking that protecting the downside would mean I could do comparably well to the stock market. I wasn’t, and it was clear I wouldn’t in the future.

The final nail in the coffin was looking at how much my portfolio grew compared to the total market since March.

Total market ~60%

My portfolio ~19% (not counting cash added)

Those numbers are crushing. I knew I had to rethink everything. And that’s where we’re at today.

If I know I’m not going to panic sell when the market drops, and have even trained myself to be excited by market drops then why am I playing so defensive? There’s no reason I can see.

So every time I get paid the portion that gets deposited into my investments goes straight to SWTSX. The next logical question is, “ why don’t you move all your holdings to that fund?” Its a good question, and one I’ve been pondering. What’s holding me back is two reasons:

- I don’t think it’s wise to make sudden sweeping changes to your investments. That kind of reactionary behavior can lead to bad habits, and I want to keep it slow.

- Given my heavy allocation of bonds I can wait for market dips and reduce my holdings at a more advantageous time.

These reasons make sense, but could also just be masking a fear of abandoning a strategy that I put so much faith into. It’s a question I will continue to ponder. Any insights or opinions are helpful!

For now I’m investing all new money into SWTSX or VTSAX, and know that it will be the best option for us in the long run. Thanks for reading, I’d love to discuss it further if you want, either in the comments or by email: mswart.ogn@gmail.com.

For the next step in our story click here. We’re going to talk about how we think about investing.